BREAKING NEWS

Yesterday, the California State Assembly voted to divest the state’s public pension funds, from coal . I have been asking Seattle’s own public pension board to consider doing the same.

. I have been asking Seattle’s own public pension board to consider doing the same.

In support of the bill, pro tem Senate President Kevin de León said:

“Coal is losing value quickly and investing in coal is a losing proposition for our retirees; it’s a nuisance to public health; and it’s inconsistent with our values as a state on the forefront of efforts to address global climate change.”

I firmly agree. We must protect our pension investments and show climate change leadership. These goals are consistent and there is more and more evidence to support this approach to fiscal and environmental stewardship.

BACKGROUND

To recap my efforts and the efforts of 350seattle.org over the last 15 months, see here:

- June 30, 2014: The City Council passes Resolution 31525, asking the Seattle City Employees’ Retirement System Board of Administration (SCERS) to work towards divestment from fossil fuel holding

- August 2014: SCERS Executive Director directed NEPC, the SCERS Board’s investment consultant, to analyze the impacts of a 5 year incremental divestment process focused upon the Carbon Underground 200, the top 100 public coal companies and the top 100 public oil and gas companies globally.

- November 2014: NEPC reported instead on the impacts of an overnight divestment. In response, I led SCERS to oppose approval of NEPC’s recommendation that SCERS not pursue fossil fuel divestment, and instead pass a motion to answer the question: “How divestment could be sequenced over the next 5 (or appropriate number of) years by refraining from making new investments in Carbon Underground 200 companies…consistent with fiduciary duties”

- February 2015: NEPC again recommended against divestment from fossil fuel companies, arguing that since no other public pension fund had divested (though public pensions outside the US have), any screening of fossil fuel companies – regardless of how gradual – would invariably reduce investment performance and increase costs.

Despite this recommendation, at the February 2015 meeting I tried to keep moving the issue further with an even more incremental approach, designed to allow SCERS investment managers to determine if and when divestment was financially prudent and address NEPC’s concerns that that changes would trigger additional transaction costs. The modest motion was: The Investment Committee recommends to SCERS the preference that, at natural points of transition, the active investment managers representing SCERS move out of fossil fuel investments with consideration of fiduciary responsibilities…”

Unfortunately, that motion failed. The motion that did pass instead was to encourage investing in alternative energy and active engagement to improve companies’ behavior, with a Quarterly Report on the state of the fossil fuel market, the progress of institutional divestment, and related ESG (environmental, social & governance) issues. Though it didn’t address the threat to our retirement funds, it is keeping this issue on the front burner. The First Quarterly Report, given in May, had a useful ten year return comparison of fossil free fund performance exceeding the performance of funds with fossil fuels. This was information that had been glossed over in the previous NEPC reports.

WHY CONSULTANTS CAN’T LEAD THE WAY

Sometimes it has seemed like NEPC has ignored studies, cherry-picked evidence, and created a narrative against divestment.

I’m learning now that financial investment consultants block advances on green investment for many structural reasons. Similarly, I’ve heard SCERS Staff and Board members remark how ESG issues cannot adequately be considered under the current structure of the Board taking the lead from our investment consultants. This study identifies several of these structural limitations. One is how a fixation of both “asset owners” and investment consultants on short term, measurable results, with the measurement of those results unfairly biasing consultants against making recommendations on issues related to green investment.

Other pension funds are starting to take actions that diverge from advice from their financial consultants. For instance, the University of Maine System, which has close to $600 million (SCERS is just twice that, at $1.2 billion) divested even though NEPC advised against it.

WHAT’S NEXT FOR THE SEATTLE EFFORT?

At our next SCERS Board meeting on Thursday, September 10, I have invited Alex Berhardt, the author of the Mercer Report to present to the SCERS Board and respond to their questions about the report. The Mercer Report is a dispassionate, but groundbreaking report from the investment community to itself, written in collaboration with “16 investment partners, collectively responsible for more than US $1.5 trillion. About the report, Mr. Berhardt has said:

“Whilst it is challenging, we have attempted to quantify the potential investment impacts of climate change. We recognize that markets do not always price in change; they are notoriously poor at anticipating incremental structural change and long-term downside risk until it is upon us.”

“Our report identifies the ‘what?’ the ‘so what?’, and the ‘now what?’ in terms of the impact of climate change on investment returns. These insights enable investors to build resilience into their portfolios under an uncertain future.”

“This report can act as a guide to creating an action plan. Whether it is setting portfolio de-carbonization targets, investing in solutions that address risks and opportunities, or increasing engagement with managers and companies, our report shows investors how they might take action. Engaging with policy makers is also crucial and helps empower investors in their role as ‘future makers.”

In addition I intend to follow up on a June request of 350.org that the Investment Committee of the SCERS Board schedule, at a future date, a discussion of how we might divesting from direct holding in coal and tar sands and consider buying a fossil free fund.

CLOSING

This campaign is part of a growing worldwide effort to divest fossil fuel investments from universities, religious institutions, municipalities, pension funds. The effort both recognizes a likelihood that:

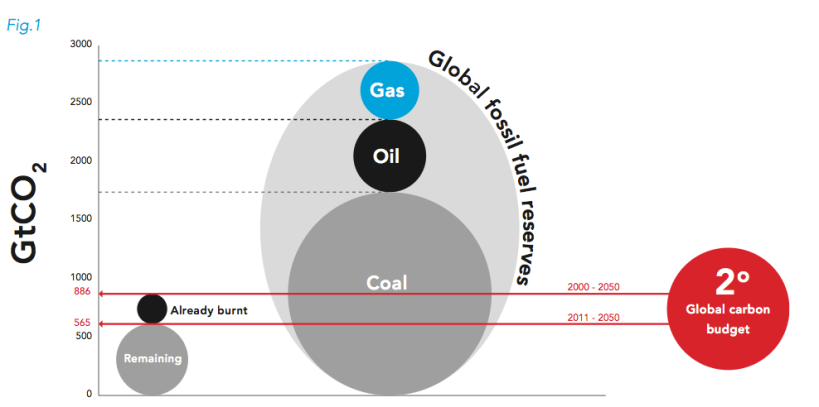

1. According to “stranded asset risk” theory, fossil fuel companies will be stuck with assets that cannot be extracted because of changing laws, regulations, or market demands, resulting in a decline in fossil fuel valuations and returns to investors.

2. The financial success of these markets and investments in them will only be realized if we continue to increase carbon fuel consumption, with devastating environmental impact.

Seattle’s participation in this campaign presents an important opportunity both to avoid financial risk and to help secure a better future for us all.